As you surely know, it is more efficient to produce larger quantities. This is the economy of scale. In a recent post I talked about the Power of Six, a rule of thumb for the relation between lead time and cost. In this post I will show you a rule of thumb for the relation between quantity and cost. Credit for this rule goes to Juan Carlos Viela.

As you surely know, it is more efficient to produce larger quantities. This is the economy of scale. In a recent post I talked about the Power of Six, a rule of thumb for the relation between lead time and cost. In this post I will show you a rule of thumb for the relation between quantity and cost. Credit for this rule goes to Juan Carlos Viela.

Economy Of Scale

The economies of scale are a well-known trend between the quantity produced and the cost per item, or more generally the cost benefits of larger enterprises. This initially applies to the entire enterprise, where larger companies can often produce more efficiently than smaller companies. However, it also applies to individual products, where producing larger quantities is likely to reduce the cost per item.

The economies of scale are a well-known trend between the quantity produced and the cost per item, or more generally the cost benefits of larger enterprises. This initially applies to the entire enterprise, where larger companies can often produce more efficiently than smaller companies. However, it also applies to individual products, where producing larger quantities is likely to reduce the cost per item.

Some of these benefits can be calculated (or more accurately, estimated) by cost accounting. Others are there but are hard to grasp quantitatively.

Some Things Accounting Can Figure Out

There are a few effects of economy of scale that accounting can figure out and quantify. Most of them are fixed costs that are spread across more products sold. Examples of these are:

There are a few effects of economy of scale that accounting can figure out and quantify. Most of them are fixed costs that are spread across more products sold. Examples of these are:

- Tool or Machine Utilization: The more parts you make with a tool or machine, the smaller the share of the cost of each part for the tools or machines.

- Development Cost: The cost to develop the product is also shared among more parts, reducing the cost per part if you produce more.

- Material Cost: Economies of scale also apply to your suppliers, and they are likely to offer you discounts for larger purchases.

- Management Overhead: The more products you make, the smaller the share of overhead cost for each part … usually. However, be aware that management costs also go up with more parts, even though they increase slower than the number of parts, as you get more overhead personnel and they may be paid more (since they manage a bigger product volume). In the worst case, you can even have a diseconomy of scale, where the overhead increases faster than the product quantity.

- Marketing: Marketing always connects only to few real customers compared to the number of people who see the advertisement. The more customers you have, the more effective your marketing.

Some Things Accounting Cannot Figure Out

Some other aspects are definitely there, but are difficult to grasp by cost accounting. Hence cost accounting usually assumes them to be zero – which they are not! See my post The Problems of Cost Accounting with Lean for more. Examples here are:

Some other aspects are definitely there, but are difficult to grasp by cost accounting. Hence cost accounting usually assumes them to be zero – which they are not! See my post The Problems of Cost Accounting with Lean for more. Examples here are:

- Worker Experience: The more parts of a certain type a worker makes, the faster he can make them. While this is true for product groups, it is also true for individual parts.

- Smaller Buffer Inventories: With larger quantities you may need a bit more buffer inventory, but the buffer inventory usually increases slower than the product quantity. Overall the cost per part will go down. See also my post How Product Variants Influence Your Inventory.

- Improved Flow: Producing more parts is likely to improve both the material flow and the information flow. This has a whole lot of synergy effects that are hard to quantify like faster detection of quality problems.

- Leveling: The more parts you make, the smaller the fluctuations in your value chain. Customer orders will be more regular, production will be smoother, and leveling will improve. Hard to quantify, but a significant effect.

It Is Bidirectional!

Please be aware that this economy of scale works in both directions. If you produce more, the cost per item is likely to go down. If you produce less, the cost per item is likely to go up.

Please be aware that this economy of scale works in both directions. If you produce more, the cost per item is likely to go down. If you produce less, the cost per item is likely to go up.

These curves are not always linear. If you need a second machine, you may have a jump in fixed costs, and until the second machine is also well utilized your cost may go up a bit with more production.

Also particularly bad is that this curve is not the same in both directions. Especially if you have to reduce your quantity, you will find out that your management overhead, number of employees, and other factors will not go down quite as quickly as you would hope. This often causes real problems for companies in a downturn.

Estimating the Effect of Volume on Cost

Juan Carlos Viela discovered a simple formula that can estimate the change in the cost of a product if the quantity changes. The formula is quite simple:

Juan Carlos Viela discovered a simple formula that can estimate the change in the cost of a product if the quantity changes. The formula is quite simple:

- ΔC is the percentage change in cost.

- ΔV is the percentage change in volume.

- k is a constant. See below for more information on this value.

For example, if you increase your volume by 10% and assume a constant k of 4, your cost per item would go down by 2.5%.

\[ { \Delta C = – \frac{\Delta V}{k} = – \frac{10 \%}{4} =-2.5\%}\]Similarly if you decrease your production volume by 10%, your cost may go up by 2.5%.

Validity

Please be aware that this is only an estimation, and the accuracy of this estimation may vary depending on your situation. Furthermore, this formula is used only for small changes in volume of up to ±20%. Hence if your production volume increases or decreases by more than 20%, the formula is no longer good.

What is my Value k?

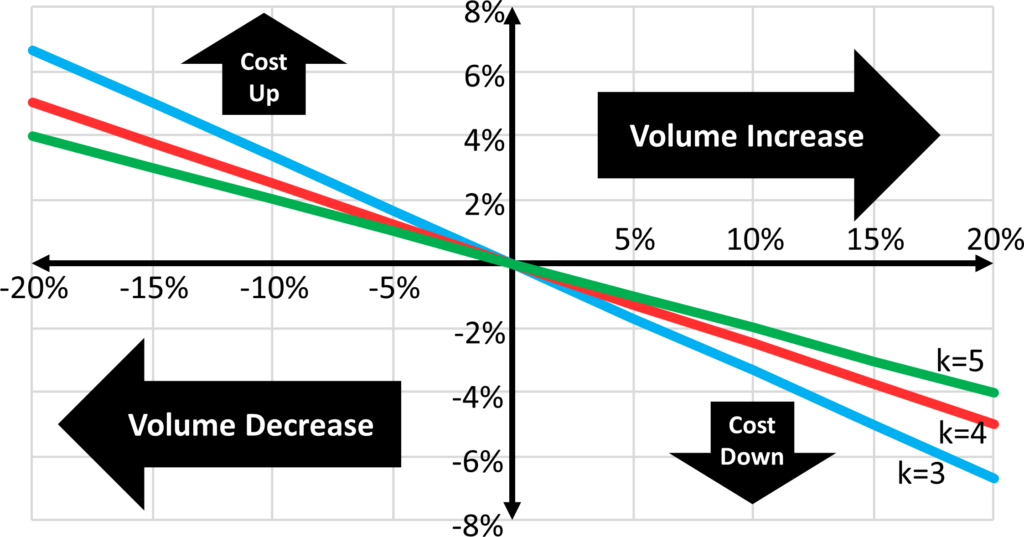

The big question of course is: What is your value of k? By experience for many cases, a value of k could be around 3 to 5. Hence your cost increases by 1/3rd to 1/5th of the volume decrease; or decreases by 1/3rd to 1/5th of the volume increase. This relation is shown in the graph below for values of k of 3, 4, and 5, showing the expected change in the cost for a change in volume.

Again, please note that this is an estimate that fits a lot of situations for quantity changes between -20% and +20%. It may not necessarily fit yours, but if you have no idea otherwise it may help as a first indicator. In any case, I hope this helps you to estimate the impact of smaller volume changes on the cost. Now, go out, get the cost down, or the volume up, or both, and organize your industry!

P.S.: Many thanks again to Juan Carlos Viela for sharing this relation and giving me permission to write about it.

You are very welcome.

Economy of scale is not a Lean approach. It’s a compromise. We have to reduce costs removing wastes not increasing volume to spread fixed costs. This is the root of birth of Lean, when Toyota realized they didn’t have have capital and market like Ford.

Hello Walter,

I disagree. We do have to reduce cost, but one way to reduce it is mass production. If everything would be custom made, you could not really afford anything anymore. One common way in lean is to reduce part/product variants to reduce prices.